Bridging the customer experience gap in payments

So, companies know payment performance and customer experience are intrinsically linked. Yet the majority are displaying a disconnect between understanding the need for a seamless experience that pushes up conversion rates and reduces churn, and then delivering it.

To bridge the gap, organisations need to consider what customers want, as reflected by how they are now expecting to pay for goods and services online and in person. They also need to ensure they offer the choice and flexibility required to stop losing revenue, and they also need a payments technology partner that can help them get it right first time, as often as possible. This drives down cost, while keeping customers happier and more loyal.

This has always been important, but it is particularly vital during the current cost of living crisis that has seen energy prices more than double and the cost of food and paying for service services hover above the general rate of inflation. More than ever before, it is critically important to ensure customers have the right payment option choices to balance income with outgoings, and to ensure payments go through first time.

How are consumers making payments?

Just a few years ago, it was sufficient for most organisations to offer a choice of credit or debit card, with the option for a Direct Debit for recurring payments, such as insurance premiums, utility bills, or gym memberships.

These are still very popular payment choices, but according to UK Finance research, Buy Now Pay Later services and the faster payments through remote banking services are proving popular. While mostly unheard of just a handful of years ago, they now collectively account for nearly a quarter of all payments in the UK.

These proportions are averaged across all payments and the percentages will vary by industry and there may be some evidence of double counting (such as BNPL being made on a card). Interestingly, organisations should be aware that UK Finance predicts that over the next ten years Direct Debit payments will be maintained at roughly the same proportion while cash will decrease in use. A major growth area will be debit and credit cards will continue to grow from 61% of all payments to 66% by 2033. Faster payments made through remote banking which will grow from just under 5 billion payments to more than 7bn payments in 2033. This is backed up by research in the Payments Journal that reveals 36% of Europeans, aged 18 to 29, now use Pay By Bank either weekly or daily.

While paying directly via a bank is a relatively new development, organisations could be forgiven for thinking that customers’ using cards is nothing new. However, to add an extra level of complexity, the UK has reached a tipping point. Government research shows that just over half (53%) of the people it surveyed in the UK now use digital wallets more than they do individual cards. This means digital wallets now account for more than a third of ecommerce sales (35%) and 10% of point-of-sale spending.

The research suggested this means organisations need to make it as simple for people to use digital wallets as their cards. The Government further suggested that the accompanying rise of Pay By Bank means business must also embrace open banking to ensure payment strategies keep pace with consumer behaviour so the industry is fit for purpose in the future.

What do customers want?

These new payment behaviours are a direct reflection of a changing expectation among the public. Prospects and customers now expect choice and so need their preferred payment method for different types of transaction to be made available – be that a digital wallet, paying via their bank directly or through a direct debit.

Customers want flexibility over payment choices, and they also require flexibility over spreading payments. Direct Debits have been in place for many years to help pay bills but now that convenience is expected in purchasing everyday items Buy Now Pay Later has grown from 12% of UK payments in 2022 to 14% in just a year.

When Access Paysuite surveyed customers towards the end of 2023, the results were crystal clear: in today’s rapidly evolving marketplace, consumer preferences for payment options and flexibility are significantly influencing their choices across various sectors. This insight underscores the growing importance of diverse payment methods in enhancing customer satisfaction and loyalty.

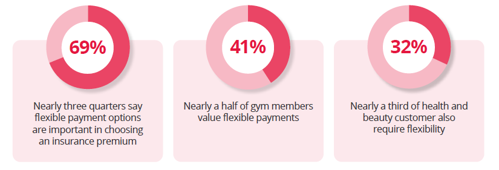

Payment choice preferences:

Payment flexibility preferences:

Payment security priorities:

Consumers want choice, to find the right payment method, and they want flexibility, to spread payments when they require. However, there is something consumers expect more than anything else - security.

It is probably not a huge surprise when one considers that, according to UK Finance, fraud accounts for 40% of all crime reported in the UK. It estimates that £1.17bn worth of fraudulent payments were made in 2023, with a rough 60:40 split between unauthorised (card details used without the owner’s knowledge) and authorised (payer duped by a criminal to send money).

That means criminals using a bank account owner or card user’s details, without their knowledge, racked up over £708m in 2023 alone. Hence, when AccessPaysuite asked consumers what features are important when considering making a payment to an organisation, there was a very clear top priority.

This is why smart organisations will always work with partners who can help reassure prospects and customers that payments are being handled securely.

Reassurance can come from displaying one of more of the prominent payment security logos, such as Visa Secure, Mastercard SecureCard or American Express SafeKey. Digital wallets form Apple, Google and PayPal are also reassuring to customers who know the two-factor authentication is there as a protective layer to prevent someone with their card details using them illegally.

What happens when customers’ payment experiences are poor?

Poor payment performance is not just a minor bump in the road that consumers can easily get over. Payment performance is central to brand image and whether a prospect converts or a customer churns.

Abandoned purchases

It is hard to gauge customer experience around payments directly because, in the case of abandoned carts and incomplete orders, reasons for not progressing are not always forthcoming. There are wild swings in the estimates for the rate at which people get to the payment stage and then quit. UK Government figures for cart abandonment suggest 30% is realistic. Some researchers, quoted by the Baymard Institute go as high as 70% to 80%.

Top reasons for aborting a payment:

- 48% - hidden costs

- 26% - requirement to set up an account

- 25% - lack of trust in payment security

- 13% - lack of preferred payment method

- 9% - declined card

Customer churn

When one considers that one in three customers in the insurance industry alone report payments not going through in the past two years (in Access Paysuite research), it becomes clear quite how big a problem failed payments are.

Failed payments cost the global economy approximately £95.3 billion annually. This is not just because of charges for failed payments and the high cost of staff dealing with them. More importantly, in terms of customer experience the research found payment failure has a detrimental impact on loyalty and, the larger the company, based on number of daily payments, the bigger the exodus:

- 60% of companies lose customers due to failed payment issues

- 80% of large companies (20,000+ payments per day) lose customers over failed payments

The customer experience disconnect - where things go wrong

Losing out on customers by not offering the right payment choice and flexible options is bad enough. But just consider this. How many organisations can afford to get their strategy right, so prospects convert, only to then let them down with the performance of their payment technology.

Not only does a poor performance in a payments system annoy customers and prompt them to churn, it can also cost businesses a huge amount of administration time trying to put things right. The result? It’s the ultimate losing situation where company resources are drained fighting a losing battle as customers leave.

To get an indication of how prevalent poor experiences are, Access Paysuite found:

In Insurance:

- 39% - had payments continue without awareness

- 35% - had trouble cancelling payments

- 33% - claim to have been overcharged

- 33% - report problems with payments not going through properly

In Financial Services:

- 50% of consumers report a problem with payments

- Failed payments, trouble cancelling, and overcharging were the biggest problems

In gym businesses:

- 24% - have had trouble with recurring payments and cancelling payments

Poor customer support:

- 32% - of financial services customers disappointed in customer service for payment queries

- 23% - dissatisfied with customer support on payment issues at gyms

How to build the frictionless service customers expect

Secure

Embracing well known security protections and displaying their icons is a crucial part of reassuring customers a payment will be handled securely.

Transparent

Be clear on pricing, including shipping and taxing, before the checkout page. Rather than calculate shipping at the last stage, be clear and upfront on delivery charges and the threshold for free delivery, if applicable. This can even encourage customers to spend a little to qualify.

Flexible, multi-channel

Legacy organisations can be picked out by only offering customers limited choices. Card options, digital wallets, pay by bank, direct debits and BNPL (on larger ticket items) need to be offered to give consumers the choice and flexibility they need to remain loyal. This comprehensive approach will ensure people can make digital payments via mobile as well as on desktop or tablets.

Go contactless

UK Government figures reveal nearly two in three debit card, and a little over half of credit card, payments are made over contactless. Any business with physical locations ignores contactless at their peril.

Embrace the telephone

Customers want the personal touch of speaking to a real person for payments (28% cite this as important in insurance payments) so it is key to work with a payment partner who can take online and mobile payments but also support telephone systems. A crucial factor here is to deploy technology that offers customers the reassuring option of keying in their payment details without having to read them out loud, or have them repeated back by a member of staff

Customer support

Executives need to be well trained on how to deal with payment queries because up to around a half of customers will have had an issue at some stage. Being able to cancel payments, build a plan to spread payments, perhaps including arrears and a commitment to putting things right, at no cost to the customer, are vital.

Cash and the digitally excluded

The 10% who use the latest digital wallets at point of sale are matched by 10% who prefer to use cash. This is not always a sign of digital exclusion, some people are paid in cash and prefer to use notes and coins. However, the 2023 Digital Exclusion Index, published by Lloyds Bank, shows that one in four people struggle to carry out digital tasks, either through lack of know-how or access to equipment and connectivity.

Embrace efficiency and excellent customer service with Access Paysuite

The customer organisations aiming to win and convert into loyal fans have no idea what is required to provide a frictionless payment experience once they press a button on a website, read their card number to an operative or set up a direct debit.

However, they do know when they do not receive the delightful experience they were expecting, and that will lead them to either not make a purchase or, if they are a customer, churn to a competitor. The payment failures that lead to this have the double-whammy of soaking up resources in what seems to be endless firefighting.

To avoid this and provide the delightful customer experience that wins new clients and engenders long-term loyalty, it is imperative that an organisation not only has the right strategy but also has the right people. They also need a best-in-class technology partner to make that strategy work for both the business and its customers.

Working with AccessPaysuite provides the required multi-channel, all-inclusive support across all channels, but it also goes a step further. The technology is set up to get it right the first time, wherever possible. Our payment success rates are among the highest in the industry, and we continually strive, behind the scenes, to automatically route a payment through an alternative fallback network if the primary choice is not working optimally. The technology works across all payment types to help an organisation remain on top of its payments strategy and ensure that surprise overpayments are avoided, so customers feel they have enjoyed a transparent payments experience.

It is this attention to detail that means customers can pay how they want over a time frame that can fit in with their requirements, and they can also expect the payment to simply go through, so they can get on with their lives.

To see what Access Paysuite can do to delight your customers and lower the cost of failure, while improving cash flow, simply click below to arrange a demo.